The eCOA Market Is About to Triple. Here's What That Means for Sponsors.

A new forecast puts the global eCOA solutions market at $7.46 billion by 2036. Here’s what that growth means for sponsors — and why the platforms that will lead it were built to run trials, not just support them.

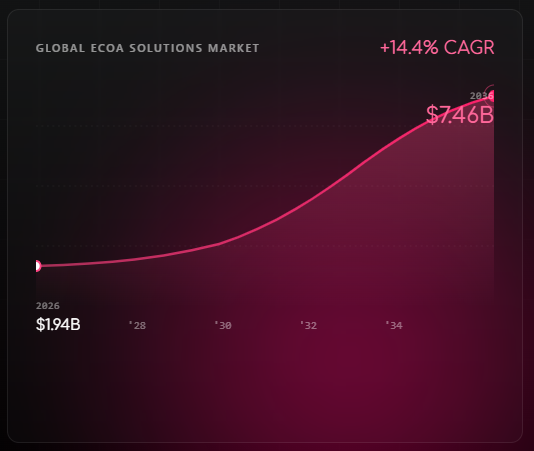

A new forecast from Research and Markets puts the global electronic Clinical Outcome Assessment (eCOA) solutions market at $1.94 billion in 2026 — on track to reach $7.46 billion by 2036. That’s a 14.4% compound annual growth rate over ten years.

For sponsors who have been slow to modernize how they capture outcome data, the window for a competitive advantage is still open. But not for long.

Why eCOA Is Growing This Fast

The report identifies four primary growth drivers, and none of them are surprises to anyone running trials today:

The shift to decentralized and patient-centric trials. Remote and hybrid trials require outcome data to travel with the patient, not wait for a site visit. ePRO and eCOA infrastructure isn’t optional in this model — it’s the foundation.

Expansion of digital health technologies. Wearables, connected devices, and AI-assisted data capture are no longer pilot experiments. They’re entering mainstream trial design, and sponsors need outcome platforms that can integrate with them without custom development work.

Regulatory support for electronic data collection. FDA and EMA guidance continues to reinforce the validity of patient-reported and observer-reported electronic data. The regulatory tailwind is real.

Demand for real-world evidence. Phase IV and RWE studies require outcome collection outside the clinical site environment, at scale, over long periods. eCOA is the only practical infrastructure for that.

Where the Market Is Headed

A few segments stand out in the forecast:

- Software leads today; services are the fastest-growing segment. Sponsors aren’t just buying tools — they need the expertise to configure, validate, and run them. Full-platform solutions with embedded support are pulling ahead of point-solution vendors.

- ePRO dominates, but eClinRO is gaining ground. Clinician-reported outcomes are increasingly being captured electronically as hybrid trial models become standard.

- Cloud-based delivery leads, but web-hosted is growing. On-premise isn’t disappearing, but the trajectory is clear.

- North America leads; Asia-Pacific grows fastest. Global trials need eCOA platforms that can operate across regions without rebuilding each time.

What This Means in Practice

A market growing at 14.4% annually is a market where the difference between the right platform and the wrong one compounds over time. Sponsors who lock in flexible, scalable eCOA infrastructure now are building a long-term operational advantage — not just solving a near-term problem.

Most eCOA vendors built software and then sold it to trial teams. ObvioHealth did it the other way around. We ran decentralized clinical trials for seven years — 60+ studies across 40 countries — before licensing ObvioGo as a platform. Every capability in it exists because we needed it to run a real study, not because a product team put it on a roadmap.

That distinction matters more as the market grows. A platform built under operational pressure handles edge cases that a purpose-built software product doesn’t anticipate. It’s also why we were able to consolidate what typically requires 4–6 separate vendors — ePRO, eConsent, participant engagement, safety monitoring, device integration — into a single no-code environment. Not by acquiring and stitching together point solutions, but because we built it as one thing from the start.

The result in practice: studies deploy in four weeks on average versus the 12–16+ weeks typical of legacy platforms. We see 91% ePRO compliance and 89% participant retention across our portfolio. And because ObvioGo is API-first, it integrates directly with Oracle Clinical One, Medidata, and Veeva — sponsors keep their existing EDC stack and just replace the participant-facing layer with something that actually works.

The market forecast confirms what sponsors running competitive trials have already figured out: fragmented vendor stacks are a liability, not a cost-saving strategy. The category is maturing, and the platforms that will lead it are the ones that were built to run trials, not just support them.